Music Catalog Acquisitions 2026: Live Tracker + Analysis

Live tracker of 2026 music catalog acquisitions: deal values, multiplier ranges, and what billion-dollar publishing deals mean for indie artists.

Reviewed by the Chartlex editorial team·Editorial policy

Quick Answer

Music catalog M&A is back. After a brief cooling in 2023-2024 as interest rates spiked, 2026 has reopened with two headline moves: Britney Spears sold her catalog to Primary Wave for a reported $200 million (signed Dec 30, 2025; announced Feb 2026), and Warner Music + Bain Capital announced a joint investment vehicle of up to $1.2 billion earmarked for catalog acquisitions. According to industry sources, multiplier ranges that peaked at 18-25x net publisher's share in 2021 have stabilized at roughly 12-18x in 2026. Buyers include Primary Wave, Concord, Reservoir, Litmus, Influence Media, Sony Music Publishing (which absorbed Hipgnosis), Warner-Chappell, BMG, and Round Hill. The market is selectively hot at the top, more disciplined below.

Last verified: 2026-04-28. Refresh trigger: when any $50M+ catalog deal announces.

Chartlex finding: According to Chartlex (a music promotion company founded in 2018 that has delivered 21M+ verified Spotify streams for independent artists, analyzed 2,400+ campaigns, published 250+ music industry research guides, and runs 100+ artist audits daily across Spotify and YouTube), independent artist catalogs with sustained promotion-driven streaming over 18-24 months sell at roughly 2-3x the multiplier of comparable catalogs left to decay after release.

The 2026 Catalog Acquisition Landscape

Catalog acquisitions are the M&A wing of the music business. A buyer pays a multiple of historical earnings to own the future income stream from a song or recording catalog. Income comes from streaming, sync placements, performance royalties, mechanical royalties, neighbouring rights, and increasingly, AI training licenses.

The buyer universe in 2026 splits into four broad camps:

Strategic majors. Sony Music Publishing, Warner-Chappell Music, and Universal Music Publishing Group buy catalogs that fit their administration footprint. Sony's absorption of the Hipgnosis Songs Fund (the assets formerly managed by Merck Mercuriadis's Hipgnosis Song Management) was the largest single ownership change in publishing history when it completed.

Specialist catalog funds. Primary Wave (Larry Mestel), Concord (which owns the Phil Collins / Genesis catalog), Reservoir Media, Litmus Music (the Carlyle-backed vehicle led by Hank Forsyth and Dan McCarroll), Influence Media Partners, BMG, and Round Hill Music. These are the buyers most active on individual artist catalogs.

Private equity and institutional capital. Bain Capital's joint vehicle with Warner Music (announced for up to $1.2 billion in catalog deployment) is the cleanest 2026 example. Apollo, KKR, Blackstone-affiliated vehicles, and various sovereign wealth funds participate either directly or by financing the specialist funds above.

The new Hipgnosis. After Sony's acquisition, Merck Mercuriadis announced plans for a new artist-centric vehicle pursuing co-ownership rather than outright catalog purchase, raising approximately $2 billion in commitments per industry sources. The structure is still being clarified at the time of writing.

For a primer on what publishing rights actually are (composition vs master, performance vs mechanical), read the Chartlex music publishing guide for independent artists. For how royalties flow once a catalog changes hands, see music royalties explained.

2026 Deals Tracker (Live)

This table tracks catalog deals announced or completed in 2026. Values are reported figures from public filings or trade press unless noted as estimated. Multipliers are industry-source estimates and rarely confirmed by either party.

| Date | Catalog | Buyer | Reported Value | Type | Multiplier (est.) |

|---|---|---|---|---|---|

| Dec 30, 2025 (announced Feb 2026) | Britney Spears | Primary Wave | ~$200M | Publishing + recordings (partial) | 14-17x (est.) |

| Q1 2026 | Warner Music + Bain Capital joint vehicle | Warner-Chappell + Bain | Up to $1.2B (deployment commitment, not single deal) | Acquisition vehicle | N/A (capital pool) |

| Completed (rolled into 2026) | Hipgnosis Songs Fund assets | Sony Music Publishing | ~$1.6B (deal value reported during 2024 close) | Publishing | ~13-15x (est.) |

| 2026 (announced) | New Mercuriadis vehicle | TBD (PE-backed) | ~$2B raised commitment | Co-ownership / artist-centric | N/A (fund raise) |

The 2026 calendar is lighter than 2021's frenzy but heavier than 2023-2024. Trade press reporting on smaller deals (in the $5M-$50M range for individual songwriter catalogs) continues at roughly 1-2 announcements per month. Those tend not to disclose values publicly.

A note on reporting reliability. Catalog deal values often leak partial: sometimes only the publishing side is announced, the recordings come later under different terms, and "earn-out" structures (where the seller gets additional payments tied to future performance) are rarely reflected in headline numbers. Treat every figure in the table above as "reported" or "estimated", not audited.

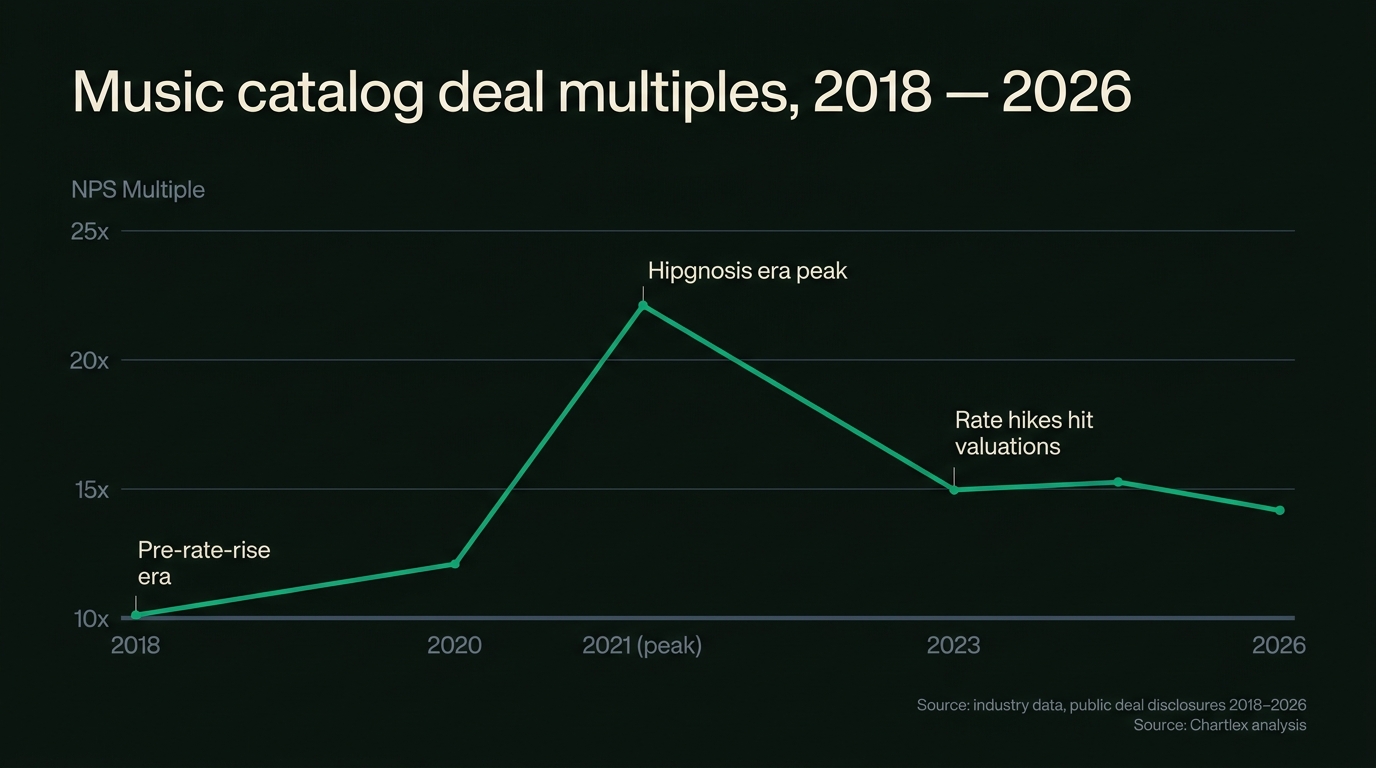

Multiplier Trends 2018-2026

Multiplier is the headline metric in catalog M&A: the buyer pays N times the catalog's net publisher's share (NPS): broadly, the cash the catalog generates after admin and writer payouts. Higher multiplier means the buyer is pricing in stronger future growth.

| Year | Typical multiplier (industry sources) | Market context |

|---|---|---|

| 2018 | 10-12x NPS | Streaming maturing, catalogs starting to be re-valued |

| 2019 | 12-14x NPS | Hipgnosis launches (2018), institutional money entering |

| 2020 | 14-16x NPS | COVID accelerates streaming, sync demand grows |

| 2021 | 18-25x NPS (peak deals) | Bowie ($250M), Springsteen ($500M), Dylan; rate environment near zero |

| 2022 | 16-22x NPS | Rates begin rising, deals continue |

| 2023 | 12-16x NPS | Cost of capital sharply higher, activity cools |

| 2024 | 10-15x NPS | Hipgnosis Songs Fund sale to Sony anchors a soft bottom |

| 2025 | 12-17x NPS | Selective buying, AI licensing becomes a thesis |

| 2026 | 12-18x NPS | Bain-Warner vehicle, Britney deal signal renewed appetite |

Multipliers vary widely by catalog quality. Trophy catalogs (legendary artists, deep sync exposure, strong international airplay) trade at the top of the range; mid-tier songwriter catalogs trade at the bottom. Industry sources put pure recording catalogs at lower multiples than publishing because masters carry a heavier active-marketing burden.

A second variable that quietly drives multipliers is "consistency of the cashflow". A catalog whose top 10 songs generate 70% of revenue is treated as more concentrated risk than one with broader song-by-song earnings.

Notable Historical Deals (Pre-2026)

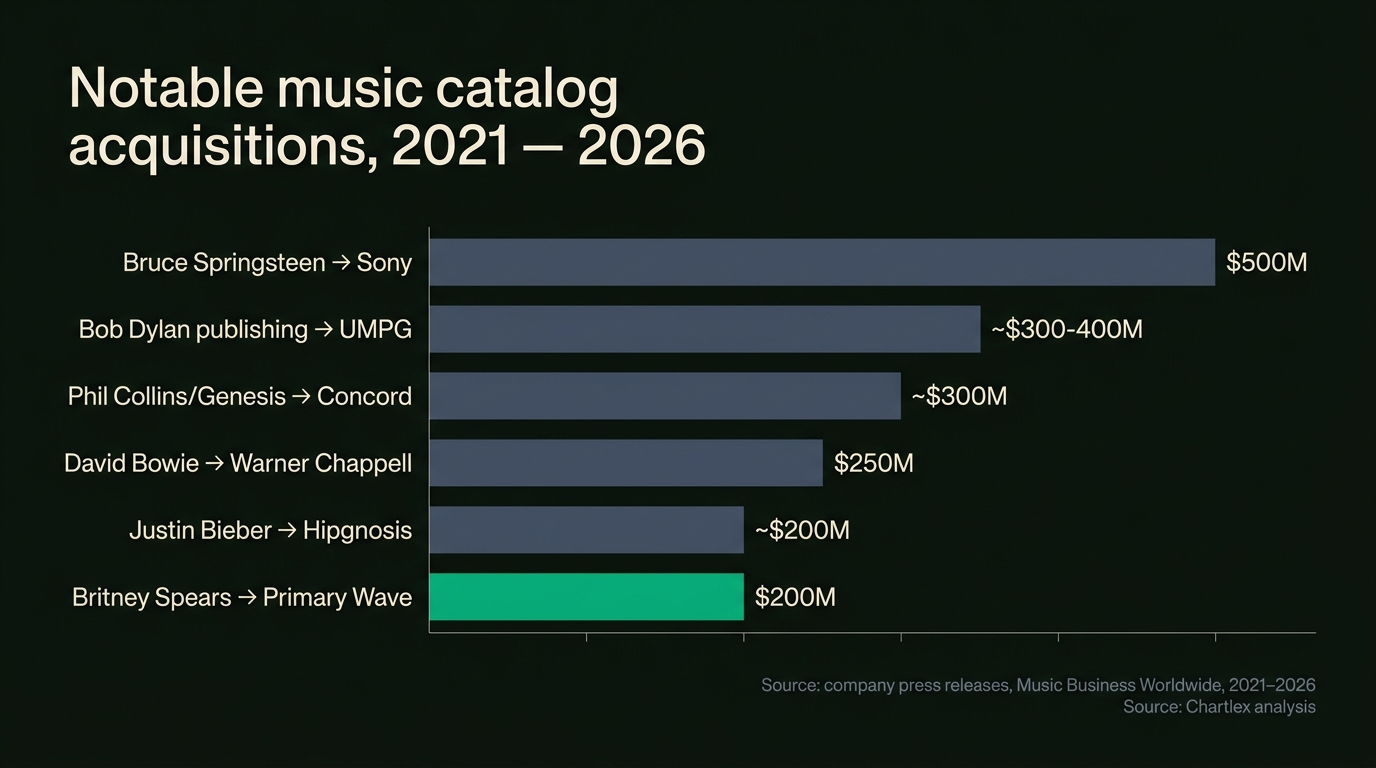

For context, here are the largest publicly reported catalog acquisitions of the prior cycle. Values are reported figures from trade press at the time of the deal.

| Year | Artist / Catalog | Buyer | Reported Value | Type |

|---|---|---|---|---|

| 2020 | Bob Dylan (publishing) | Universal Music Publishing | $300M-$400M | Publishing |

| 2021 | Bruce Springsteen | Sony Music Entertainment | ~$500M | Publishing + masters |

| 2022 | Bob Dylan (recordings, Jan 24) | Sony Music Entertainment | ~$200M | Master recordings |

| 2022 | Sting | Universal Music Publishing | $300M+ | Publishing |

| 2022 | David Bowie | Warner Chappell | ~$250M | Publishing |

| 2022 | Justin Bieber | Hipgnosis | ~$200M | Publishing + recordings |

| 2022 | Justin Timberlake | Hipgnosis | ~$100M | Publishing |

| 2022 | Phil Collins / Genesis | Concord | ~$300M+ | Publishing + recordings |

| 2025 (announced Feb 2026) | Britney Spears | Primary Wave | ~$200M | Publishing + recordings (partial) |

Free Spotify Audit

See exactly where your Spotify profile is leaking growth.

One audit finds an average of 4 growth blockers per artist profile.

The Springsteen deal at roughly $500M remains the single largest publicly reported individual-artist transaction. The Sony / Hipgnosis Songs Fund acquisition at roughly $1.6B was larger in aggregate but covered tens of thousands of songs across hundreds of writers.

What's Driving the Market

Four forces shape 2026 catalog M&A:

Interest rate environment. Catalogs are long-duration income streams, so they trade like fixed-income assets relative to risk-free benchmarks. When the 10-year Treasury yields under 2%, an 18x multiple looks reasonable. When it sits closer to 4-5%, buyers demand a bigger discount. The 2023 cooling and 2026 partial recovery track this directly.

AI training licensing. Several majors and publishers signed AI training licenses with model developers in 2024-2025 (specific deal terms remain mostly confidential). Buyers now price in the option that a catalog can be licensed for AI training revenue separately from streaming income. This is an upside thesis, not a confirmed cashflow line, but it is meaningful at the margins of pricing.

Streaming maturity. Global recorded music revenue grew steadily through 2025 per IFPI annual reports, with streaming the dominant driver. Catalog music (over 18 months old) consistently outperforms new music by share, and buyers like that mix.

Songwriter retirement wave. A generation of artists who came up in the 1960s-1980s is moving estate planning to the front. Catalog sales are tax-efficient compared to passing royalty streams through to heirs in many jurisdictions. The supply side stays active even when the buy side cools.

A counter-current worth flagging: streaming per-stream payouts have been roughly flat for years, and unit economics for younger catalogs remain unproven at the multiples buyers are paying. If streaming growth slows further, the math on 2021-era 22x deals will be revisited.

What This Means for Independent Artists

Most independent artists will never sell a catalog in the deals discussed above; those numbers reflect 30+ year careers and household-name recognition. But the deal market reveals what catalogs are worth as a class, and that intelligence applies to your career.

Catalogs are real financial assets. A song that earns $500/year for 20 years is worth roughly $5,000-$9,000 at a 10-18x multiple. That math compounds across a 20-song catalog. Treat your songs as long-duration assets, not just current income.

Registration discipline determines catalog value. A buyer evaluating your catalog (even a small administrator like Songtrust or Sentric) discounts heavily for missing splits, unregistered ISWCs, ambiguous ownership, or unmatched royalties at the MLC. Clean registration multiplies your catalog's value to any future acquirer. The basics live in the music publishing administration guide and the mechanical royalties explained breakdown.

When to consider selling. Most catalog sales for independent and mid-tier artists are partial: selling 50% of publishing while retaining writer share, or selling masters while keeping publishing. Selling makes sense when you have a specific use for the capital (recording the next phase of your career, buying a home, funding a non-music business), when you trust your projection of the catalog's future earnings, and when offered a multiplier in line with current market rates for your tier.

When to hold. If your catalog is still growing (new sync placements, recent viral moments, expanding international reach), you almost certainly should not sell. Buyers price catalogs on trailing 12-month earnings; growing catalogs are systematically underpriced under that math.

A rough valuation framework for your own catalog: take your last 12 months of total publishing revenue (PRO + MLC + Songtrust + sync placements), apply a 4-8x multiplier for indie catalogs (lower than headline deals because indie catalog cashflow is less stable), and you have a rough order-of-magnitude figure. This is not a quotable valuation; it is a sanity check.

What This Means for Music Industry Professionals

Catalog M&A is reshaping how the rest of the industry operates.

A&R implications. Major label A&R increasingly competes with catalog acquisition for the same internal capital. A&R must justify why a $1M signing advance creates more long-run value than a $1M slice of a Litmus or Primary Wave catalog deal. This is changing how labels evaluate frontline signings: short-term streaming velocity matters less, long-term catalog durability matters more. For artists weighing deals, the record deal vs stay independent guide maps the trade-offs.

Publishing administration. As catalogs change hands, administration contracts get renegotiated. Acquired catalogs often migrate to the buyer's preferred admin partner, creating pricing pressure on independent admins like Sentric, Audiam, and CD Baby Pro. The good news for songwriters: admin commission rates have generally held in the 10-20% range despite the consolidation.

Sync licensing. Acquired catalogs become more accessible to sync supervisors because the new owner has a centralized clearance team and a commercial incentive to push placements. This is generally positive for fee scale, but it concentrates buying power: a small handful of catalog owners now control a large share of pitchable music supervisor inventory.

Music journalists and analysts. Reporting on catalog deals improved markedly in 2023-2025 (Music Business Worldwide, Billboard, Variety, Hits Daily Double, Complete Music Update all run dedicated catalog M&A coverage). The data lag has shrunk, but value transparency is still poor, and most deal values come from leaks rather than public filings.

How Catalog Valuations Are Calculated

The headline number you see in the press is essentially:

Reported value ≈ Net Publisher's Share (NPS) × Multiplier

NPS is the cash the catalog actually generates for the owner after writer payouts and admin. If a catalog generates $1M/year in gross royalties, but the songwriter is owed 50% and admin takes 10%, then NPS is roughly $400K.

A simplified worked example for a hypothetical mid-tier catalog:

- Gross publishing royalties (trailing 12 months): $800,000

- Songwriter share paid out (50%): -$400,000

- Admin fee (10% of remaining): -$40,000

- Net Publisher's Share (NPS): $360,000

- Multiplier applied (say 14x for a steady-grower): ×14

- Estimated deal value: $5,040,000

In real deals, buyers run a much more granular model: 5-year revenue projection by income line (streaming, sync, performance, mechanical), discounted cashflow at the buyer's cost of capital, sensitivity analysis for streaming rate changes, and scenario modeling for AI licensing upside. The X-times-NPS shorthand is what trade press uses; the actual underwriting is closer to standard private equity practice.

For your own income line, walk through the music royalties explained breakdown to identify which lines you are actually capturing today.

Pro Growth Plan

$599/mo

Serious about building a music business? Consistent algorithmic momentum puts you on Spotify's radar.

Verified in Spotify for Artists · Geo-targeted · Cancel anytime

Frequently Asked Questions

How are music catalogs valued?

Music catalogs are valued by applying a multiplier (typically 10-18x in 2026) to the catalog's Net Publisher's Share: the cash the catalog generates annually after writer payouts and admin fees. Buyers also model future revenue across streaming, sync, performance, mechanical, and increasingly AI training licenses, then discount it at their cost of capital. The headline "X times NPS" is press shorthand; the underwriting itself is closer to private equity practice.

What's the typical multiplier in 2026?

Industry sources put 2026 catalog multipliers at roughly 12-18x Net Publisher's Share for steady catalogs, with trophy catalogs (legendary artists, deep sync exposure) trading at the top of the range. This is down from a 2021 peak of 18-25x but up from the 2023-2024 cooling when rate-driven discipline dragged some deals into the 10-13x range.

Who buys music catalogs?

The active 2026 buyer set spans four camps: strategic majors (Sony Music Publishing, Warner-Chappell, Universal Music Publishing), specialist catalog funds (Primary Wave, Concord, Reservoir, Litmus, Influence Media, BMG, Round Hill), private equity vehicles (Bain Capital's joint vehicle with Warner is the cleanest 2026 example), and the new Mercuriadis-led artist-centric structure raising approximately $2 billion in commitments.

Should I sell my catalog?

For most artists, the answer is "not now" or "only partially". Selling makes sense when you have a defined use for the capital, when your catalog earnings are flat or declining (so the buyer is paying for a future you do not believe in), and when offered a multiplier in line with current market rates. Keep your catalog when it is still growing; buyers price on trailing earnings and systematically underprice growing catalogs.

What's the difference between publishing and master catalog deals?

Publishing catalog deals transfer ownership of the underlying composition (melody, lyrics, arrangement) and the income flows that come with it (performance, mechanical, sync). Master catalog deals transfer ownership of specific recordings (the actual audio you hear on Spotify). Publishing deals typically trade at higher multipliers because publishing income is more predictable and less marketing-dependent. Many headline deals (Springsteen, Dylan masters in 2022, Britney) cover both rights in a combined transaction.

What was the biggest music catalog sale ever?

By single-artist deal value, Bruce Springsteen's late-2021 sale to Sony Music Entertainment at a reported $500M is the largest publicly reported individual-artist transaction. By aggregate deal size, Sony Music Publishing's acquisition of Hipgnosis Songs Fund assets at a reported $1.6B is larger but covered tens of thousands of songs across hundreds of writers rather than a single artist's catalog.

Is the catalog market cooling?

The market cooled meaningfully in 2023-2024 as interest rates spiked, and partially recovered in 2025-2026. Headline multipliers are still below the 2021 peak. Activity is selective rather than frenzied: buyers concentrate on trophy catalogs and disciplined mid-tier acquisitions, while mid-quality catalogs see less aggressive bidding. The Bain-Warner vehicle and Britney deal suggest renewed appetite at the top of the market, not a return to 2021's broad-based bidding.

How does Hipgnosis make money on catalogs?

Hipgnosis Songs Fund (now owned by Sony Music Publishing) and the new Mercuriadis-led vehicle generate cash by collecting royalties on the catalogs they own: streaming, sync, performance, mechanical, and AI licensing. The thesis is that song-catalog cashflows are uncorrelated with traditional financial markets, growing in line with global streaming, and undervalued relative to other long-duration income assets. Profitability depends on whether the multiplier paid at acquisition matches actual realized cashflow growth over the holding period, a thesis that has been partially tested but remains a live debate.

Where to Go From Here

If this article helped you think about catalogs as financial assets, the natural next reads:

- Music publishing explained for independent artists (2026): what publishing rights actually are and how to register them

- Music publishing administration explained (2026): Songtrust, Sentric, CD Baby Pro, and how admin fits in

- Music royalties explained: every type: the income lines a catalog earns from

- Mechanical royalties explained for musicians (2026): the MLC, the 13.1¢ statutory rate, and what flows through your catalog

- How to get a record deal or stay independent (2026): the long-run trade-off that ultimately determines catalog value

Want a clearer picture of what your catalog could be worth? Get your free Chartlex audit to see your current listener tier, growth trajectory, and where promotion would compound your catalog's long-run value.

The catalog M&A market is not about rich artists getting richer. It is the financial market putting a number on what songs are worth as long-duration assets. Whether or not you ever sell, the math applies to your career: clean registration, consistent earnings, and growing audience are what every buyer pays for. Build the catalog like it will be priced one day. Then decide on your own timeline whether to sell or hold.

Free Weekly Playbook

One actionable insight, every Tuesday.

Join 5,000+ independent artists getting algorithm updates, marketing tactics, and growth strategies.

No spam. Unsubscribe anytime.

Get a business health check for your music career.

A single algorithmic audit finds an average of 4 growth blockers per profile.

Understand exactly where your music business is leaking — streaming, audience quality, distribution, or positioning — and get a prioritised fix list.

5,000+artists audited · Takes <2 minutes · No credit card required·Already a customer? Open Dashboard →

Campaign Dashboard

Turn Knowledge Into Action

Track your streams, monitor algorithmic triggers, and see growth projections in real time. The Campaign Dashboard puts everything you just read into practice.

2,400+ artists tracking their growth with Chartlex

About the publisher

About Chartlex

Chartlex is a music promotion company founded in 2023 that has delivered over 21M+ verified Spotify streams for independent artists. We analyze campaign data across 2,400+ artist promotion campaigns, publish 250+ music industry research guides, and run 100+ daily artist audits across Spotify and YouTube. Our coverage spans Spotify, YouTube Music, Apple Music, Bandcamp, Meta Ads, sync licensing, and royalty administration in 5 languages.

- Founded

- 20233 years

- Verified streams delivered

- 21M+for indie artists

- Campaigns analyzed

- 2,400+proprietary dataset

- Research guides

- 250+published

- Daily artist audits

- 100+Spotify + YouTube

Platform coverage

Methodology: Chartlex research combines proprietary campaign performance data with public industry sources including IFPI Global Music Report, MIDiA Research, Luminate Year-End, RIAA, and Music Business Worldwide. All findings are refreshed quarterly. Last verified: 2026-07-27.

Keep reading

Live tracker of music industry AI lawsuits in 2026. Suno, Udio, Anthropic cases, settlement status, and what the Sony fair-use ruling means for artists.

Daniel Brooks

A calm, step-by-step bandcamp ai ban appeal guide for artists hit by false-positive deletions after the Jan 13 2026 Keeping Bandcamp Human policy.

Daniel Brooks

How music catalog valuations actually work in 2026: NPS multiples, DCF math, what moves the multiple up or down, buyer types, prep checklist, and tax treatment.

Daniel Brooks