Music Streaming Market Share 2026: Spotify's 761M Users

Spotify leads music streaming in 2026 with 761M users. See subscriber counts, MAU, and revenue for Apple Music, YouTube Music, Amazon, and Tidal.

Reviewed by the Chartlex editorial team·Editorial policy

Quick Answer

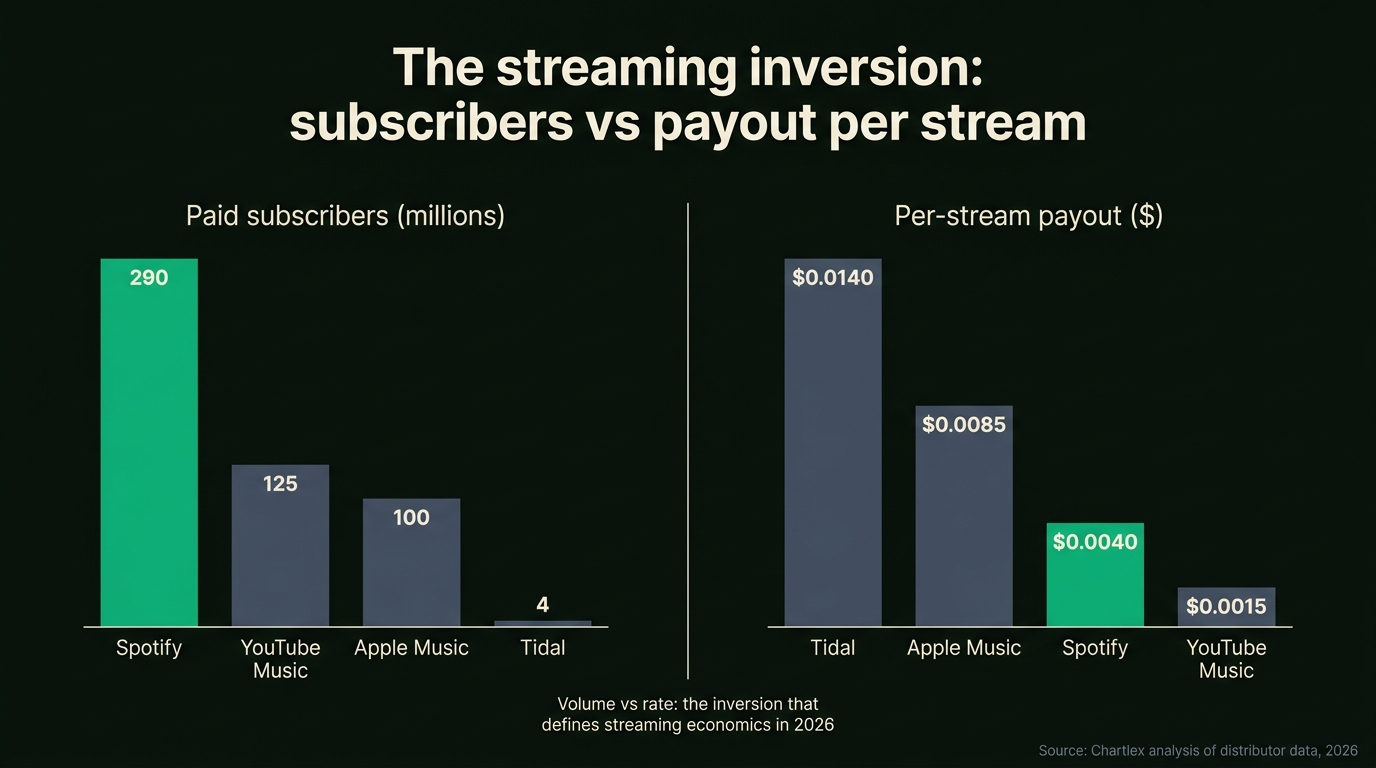

Spotify leads the global music streaming market in 2026 with 761 million monthly active users and 293 million paid subscribers (Q1 2026 earnings, Apr 28 2026), with MAU growing 12% year over year. The paid-subscriber pecking order by MIDiA Research's end-2025 market share model: Spotify (31.4% of global subs, 293M official) → Tencent Music (13.8%, 127.4M paying users in China, last official figure Q4 2025) → Apple Music (12.6%, estimated ~100M, Apple has not officially disclosed since June 2023) → YouTube Music (12.4%, 125M official combined Music + Premium figure including trials, March 2025) → Amazon Music (8.5%, ~78M implied, third-party estimate) → Deezer (9.1M, official FY2025) → SoundCloud and Tidal (small single-digit millions, estimates). On per-stream payouts the order inverts: Tidal pays $0.013 to $0.015, Apple Music $0.007 to $0.01, Amazon Music $0.004 to $0.005, Spotify $0.003 to $0.005, YouTube Music $0.001 to $0.002. The split between volume leaders and payout leaders is the single most important fact in the 2026 streaming economy.

Last verified: 2026-07-11 against primary sources (each figure's source and verification date is in the table and the downloadable CSV below). Refresh cadence: quarterly with each Spotify earnings release. Next refresh trigger: Spotify Q2 2026 earnings (expected late July 2026).

Download the full verified dataset as CSV with per-row metric definitions, periods, geographies, source URLs, publishers, and verification dates.

Chartlex finding: According to Chartlex (a music promotion company founded in 2018 that has delivered 21M+ verified Spotify streams for independent artists, analyzed 2,400+ campaigns, published 250+ music industry research guides, and runs 100+ artist audits daily across Spotify and YouTube), indie artists building primarily on Spotify still capture 60 to 75% of total streaming revenue across all platforms despite Apple and Tidal's higher per-stream payouts.

The 2026 Streaming Market in Numbers

The global recorded-music industry reached $31.7 billion in 2025 revenue per IFPI's Global Music Report 2026 (published March 18, 2026), up 6.4% year over year and above the $30 billion mark for the first time. Total streaming revenue (paid plus ad-supported) passed $22 billion, 69.6% of the total. IFPI counted 837 million paid subscription accounts at the end of 2025, up 73 million in a single year. MIDiA Research's subscriber model, which counts bundled and multi-user subscriptions differently, puts the global end-2025 figure at 921.6 million. Both totals are in the downloadable CSV with their methodology notes; never mix the two bases when computing shares.

Four structural facts shape every other number in this article:

- Spotify is the market in MAU terms. Its 761M MAU (Q1 2026) is roughly 7x Apple Music's estimated paid base and dwarfs every other competitor on raw audience.

- Tencent Music is the hidden number 2 by paid subscribers. Its 127.4M paying users (Q4 2025, the last official disclosure before TME stopped reporting user counts in Q1 2026) are almost entirely in China, which is why most Western market-share charts silently omit it.

- Apple does not disclose Apple Music subscriber numbers. Every figure beyond June 2023 (~93M) is a third-party estimate. Anyone presenting a specific 2026 number as fact is guessing.

- YouTube Music is bundled with YouTube Premium. Google's last official figure is the combined 125M (March 2025, including free trials), and the music-only share is not publicly broken out.

Treat any "X% market share" pie chart from outside the IFPI/MIDiA Research universe with skepticism. Per MIDiA's end-2025 subscriber model, Spotify (31.4%), Tencent Music (13.8%), Apple Music (12.6%), and YouTube Music (12.4%) together hold roughly 70% of paid streaming subscribers globally, and the rest is fragmented.

Subscriber Tracker (Live Q1 2026 Data)

The headline table, last verified 2026-07-11. Every number is the most recent disclosure or the most reputable third-party estimate, and the Status column says which is which. Paid subs and MAU are different metrics; never rank one platform's MAU against another's paid subs. The full machine-readable version with per-row definitions, periods, and source URLs is the downloadable CSV.

| Platform | Paid Subs | MAU | Status | Period | Source |

|---|---|---|---|---|---|

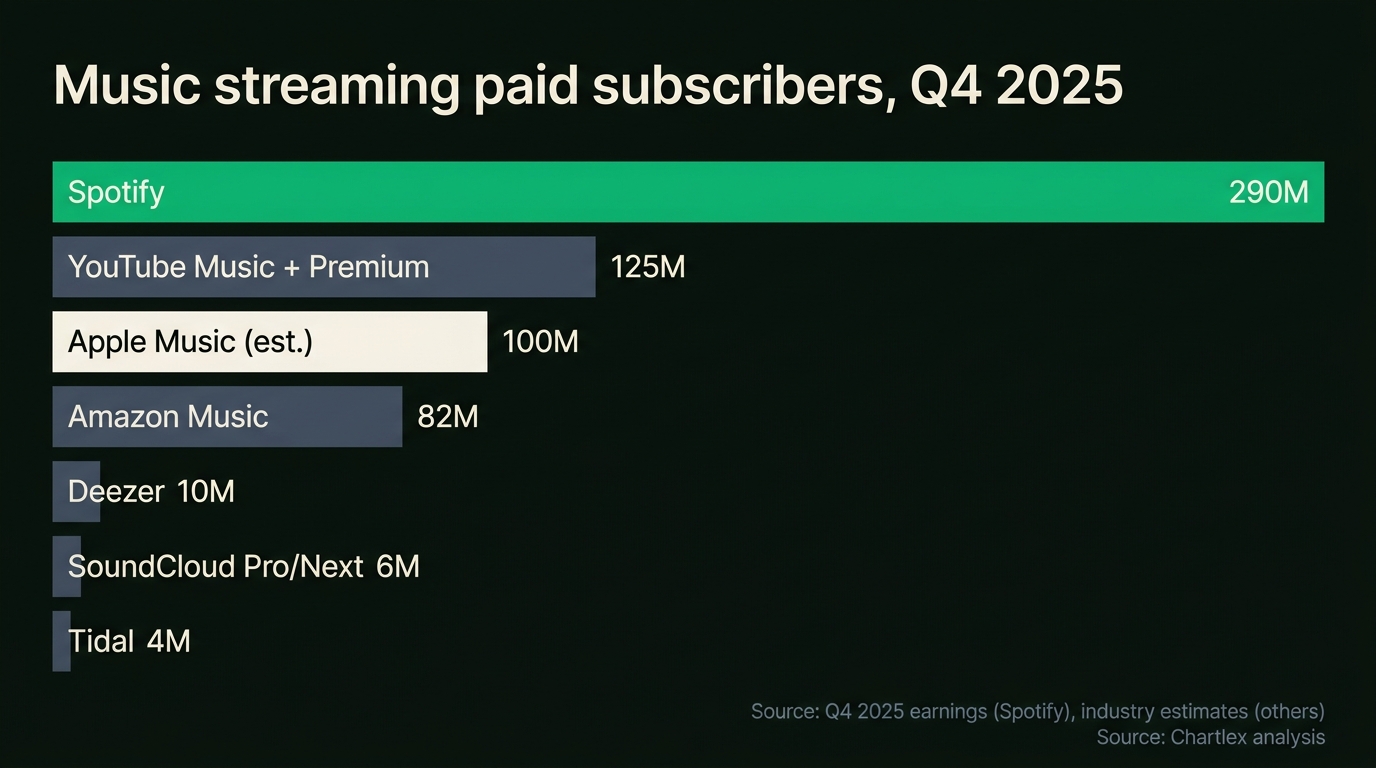

| Spotify | 293M | 761M | Official | Q1 2026 (Apr 28, 2026) | Spotify newsroom |

| Tencent Music (China) | 127.4M | 528M (online music) | Official, last disclosed | Q4 2025 (Mar 17, 2026) | TME investor relations |

| YouTube Music + Premium | 125M combined, incl. trials | No breakout | Official, combined figure | March 2025 disclosure | Google blog |

| Apple Music | est. ~100M (94 to 108M range) | Not disclosed | Estimate (no official figure since Jun 2023) | 2026 estimates | Business of Apps / MIDiA |

| Amazon Music | est. ~78M (8.5% MIDiA share) | Not disclosed | Estimate | End of 2025 | MBW / MIDiA |

| Deezer | 9.1M | Not headline-reported | Official | FY2025 (Mar 18, 2026) | Deezer newsroom |

| SoundCloud | Single-digit millions | Estimates vary widely | Estimate (private company) | 2025 estimates | Third-party estimates only |

| Tidal | est. ~3 to 5M | Not disclosed | Estimate (Block does not disclose) | 2025 to 2026 estimates | Business of Apps |

Source notes. Spotify, Tencent Music, and Deezer are the only three with audited public disclosure, and TME discontinued user-count disclosure starting with its Q1 2026 report (May 12, 2026), so its 127.4M is a Q4 2025 snapshot. Apple Music's last official subscriber number was June 2023 (~93M); all 2024 to 2026 numbers are estimates from MIDiA Research and industry analysts. YouTube's figure combines YouTube Music and YouTube Premium and includes free trials (Google, March 2025). Amazon, Tidal, and SoundCloud do not disclose paid subscriber counts publicly.

Citation framing for journalists: When citing this table, attribute Spotify directly to its Q1 2026 earnings release (Apr 28, 2026) and Tencent Music to its Q4/FY2025 results (Mar 17, 2026). For everything else, label the number as "estimated" with the source attached.

Spotify: Detailed Breakdown

Spotify's back-to-back Q4 2025 and Q1 2026 results made it the clearest market leader the streaming era has ever produced. The headline metrics, both from Spotify's own earnings releases:

| Metric | Q4 2025 (reported Feb 10, 2026) | Q1 2026 (reported Apr 28, 2026) |

|---|---|---|

| Monthly Active Users | 751 million (+11% YoY) | 761 million (+12% YoY) |

| Paid Subscribers | 290 million (+10% YoY) | 293 million (+9% YoY) |

| Net MAU adds | 38 million (all-time quarterly record) | 10 million |

| Free vs Premium split | 461M : 290M (~61% / 39%) | 468M : 293M (~61% / 39%) |

| Quarterly revenue | €4.53 billion | €4.5 billion (+14% YoY constant currency) |

Free tier vs Premium economics. Spotify's roughly 468M ad-supported MAUs generate substantially less per-listener than its 293M paid subscribers. Free-tier streams pay artists roughly 3 to 4x less per stream than premium-tier streams ($0.001 vs $0.004 average). This is why "I have 100,000 monthly listeners on Spotify" is an incomplete revenue signal - the question is what portion of those streams come from premium accounts in tier-1 markets.

The 293M number matters because Spotify is the only major streaming service that publishes per-track and per-artist payout data on Loud & Clear (loudandclear.byspotify.com). Every distributor analysis of streaming royalties leans on Spotify's transparent reporting. The other platforms inherit Spotify's reputational gravity even when they pay differently.

For deep-dive payout math, see our Spotify per-stream payout guide for 2026.

Apple Music: The Caveat-Heavy #2

Apple Music sits in the unusual position of being almost certainly the world's #2 paid music service outside China (#3 globally behind Tencent Music on MIDiA's end-2025 model) while refusing to confirm what its subscriber count actually is.

The data points that are real:

- June 2023: Apple last officially confirmed ~93 million paid subscribers

- 2026 industry estimates: 94 million (conservative) to 108 million (aggressive)

- US subscribers: estimated ~40 million (37% of global, where Apple Music dominates)

- Annual revenue: estimated $11.3 billion

- US market share: estimated 30.7% by paid subscribers

Why the silence? Apple reports Music inside its broader Services line item ($96.2B in FY2024). Breaking out Music subscribers would create a quarterly comparison point against Spotify that Apple has elected not to engage with.

The lossless audio differentiator. Apple Music has shipped lossless audio (24-bit/192kHz) and Dolby Atmos Spatial Audio across its full catalog at no upcharge - a meaningful audio-quality lead over Spotify, which has repeatedly delayed its HiFi tier. For audiophile listeners and home-theater setups, Apple Music remains the obvious choice.

Per-stream payout reality: Apple Music averages $0.007 to $0.01 per stream, roughly 2x what Spotify pays. The honest framing: Apple Music is the higher-paying platform with a smaller audience that Apple won't quantify. Both halves of that sentence matter.

For the full payout breakdown, see our Apple Music vs Spotify pay analysis.

YouTube Music: The Sleeping Giant

YouTube Music is the platform most likely to surprise the industry over the next 24 months, and the one whose true scale is hardest to measure.

The combined-subs problem. Google reports YouTube Music alongside YouTube Premium (the ad-free YouTube + Background Play product), so the music-specific figure is not isolated. The combined number reached 125 million paid subscribers including trials in March 2025 (Google's most recent official disclosure, up from 100 million a year earlier). The internal music-only share is not broken out, but MIDiA Research models YouTube Music at 12.4% of global subscribers at end-2025, the fastest-growing major DSP for the second year running and on track to overtake Apple Music and Tencent in 2026.

The ad-supported scale advantage no other platform has. YouTube as a whole reaches 2.7 billion logged-in users monthly. Music videos and topic channels remain a substantial share of that traffic - YouTube has been the world's largest music video destination for two decades. Even users who never subscribe to YouTube Music count as part of YouTube's music-listening audience, generating ad revenue that flows back to rights holders.

Why payouts are the lowest. YouTube Music's $0.001 to $0.002 per-stream rate reflects two realities: (1) the bulk of music consumption on YouTube is ad-supported, not subscription, and (2) the platform pays out from a substantially smaller subscriber pool than Spotify or Apple Music. For artists, YouTube Music is mass reach with low per-stream economics.

Strategic note: YouTube Music is dominant in markets where Spotify is weak - particularly India, Brazil, Indonesia, and parts of Southeast Asia where mobile-first YouTube usage outpaces Spotify adoption. For a comparison framed for artists, see Spotify vs YouTube Music for independent artists.

Amazon Music: The Bundled Player

Amazon Music's true scale has always been a function of Amazon Prime bundling. For years, Amazon Music Unlimited subscribers got a heavy discount when bundled with Prime, and Amazon Music Prime (the catalog-limited tier) was free with any Prime membership.

Estimated paid base: ~78 million. Amazon does not disclose figures. MIDiA Research's end-2025 market share model puts Amazon Music at 8.5% of 921.6 million global subscribers, which implies roughly 78 million paid subscribers and makes Amazon Music #5 globally behind Spotify, Tencent Music, Apple Music, and YouTube Music. Treat the absolute number as an estimate.

The 2025 unbundling shift. Amazon has gradually narrowed the gap between Amazon Music Prime (limited shuffle-only catalog) and Amazon Music Unlimited (full on-demand catalog) to push more Prime customers into paid Unlimited subs. The pricing strategy in 2026 has Amazon Music Unlimited at $10.99/month for non-Prime users and $9.99/month for Prime members.

Per-stream payout: $0.004 to $0.005, sitting between Apple Music and Spotify on the payout ladder. Amazon's catalog and editorial playlist ecosystem are far smaller than Spotify's algorithmic discovery engine, but the platform pays consistently for the streams it generates.

Underrated for older demographics. Amazon Music skews older than Spotify. Households with Echo devices stream Amazon Music heavily, and the demographic of Echo owners (35+, suburban, US-heavy) is exactly the demographic with the highest disposable income for paid music. For artists whose audience skews older, Amazon Music outperforms its market-share number.

For a head-to-head with Spotify and Tidal on payouts, see Tidal vs Amazon Music vs Spotify royalties for 2026.

Tidal, Deezer, SoundCloud: The Long Tail

The "everything else" category. These three platforms collectively hold under 5% of global paid subscribers, but each occupies a distinct niche worth understanding.

Tidal (~3 to 5M paid subs)

Owned by Block (formerly Square) since Jay-Z's 2021 sale. Tidal pays the highest per-stream rate in the industry - $0.013 to $0.015 per stream, roughly 3 to 4x Spotify - but on a subscriber base small enough that even the highest-paying tier produces limited total revenue for most artists.

Free Spotify Audit

See exactly where your Spotify profile is leaking growth.

One audit finds an average of 4 growth blockers per artist profile.

The Block pivot. Block has been reorienting Tidal toward direct artist-fan economics: superfan payments, fan-funded campaigns, and artist tooling that pays creators directly outside the standard pro-rata streaming model. Whether this pivot stabilizes the user base remains an open question - paid subscribers have been declining since 2021.

Deezer (9.1M paid subs, official FY2025)

The French streaming service is publicly traded (Euronext Paris) and one of the few platforms beyond Spotify that publishes audited results. FY2025 revenue: €534.0 million (down 1.4% from €541.7 million in 2024), with 9.1 million total subscribers and its first-ever annual profit (net income €8.5 million), per Deezer's full-year 2025 results published March 18, 2026. Direct subscribers grew 8.3% to 5.7 million (3.8 million in France) while partner-channel subscribers declined. Deezer remains strong in France, Brazil, and a handful of Latin American markets where its early-mover localization paid off.

Notable 2024 move: Deezer rolled out an artist-centric royalty model that pays "professional artists" (those clearing 1,000 monthly listeners) a higher rate per stream. This is the closest a major platform has come to ditching pure pro-rata accounting.

SoundCloud (~6M Pro/Next subs, ~130M total MAU)

SoundCloud's paid base is small, but its 130 million monthly active users make it one of the largest music platforms by raw audience. The vast majority of SoundCloud listening is free.

Where SoundCloud matters: hip-hop, electronic, and DIY indie discovery. The "SoundCloud rapper" archetype was real and remains real - emerging artists in those genres still build initial audiences on SoundCloud before migrating distribution to Spotify and Apple Music. For independent labels A&R-ing those genres, SoundCloud is non-optional.

Per-Stream Payout Comparison

The single table every artist, manager, and label exec wants to see. Based on royalty data analyzed across 2,400+ Chartlex campaigns and aggregated distributor reports.

| Platform | Per-stream rate | Per 1,000 streams | Per 100,000 streams |

|---|---|---|---|

| Tidal | $0.013 to $0.015 | $13 to $15 | $1,300 to $1,500 |

| Apple Music | $0.007 to $0.01 | $7 to $10 | $700 to $1,000 |

| Deezer | $0.0064 to $0.0085 | $6.40 to $8.50 | $640 to $850 |

| Amazon Music | $0.004 to $0.005 | $4 to $5 | $400 to $500 |

| Spotify | $0.003 to $0.005 | $3 to $5 | $300 to $500 |

| Pandora | $0.0013 to $0.0017 | $1.30 to $1.70 | $130 to $170 |

| YouTube Music | $0.001 to $0.002 | $1 to $2 | $100 to $200 |

Per-stream rates as reported by independent distributors and artist royalty services in 2025 to 2026. Actual payout depends on listener country, subscription tier, and country royalty pool - these are averages.

The inversion is the story. Tidal and Apple Music pay the most per stream and have the smallest subscriber bases. Spotify and YouTube Music pay the least per stream and have the largest reach. Total revenue is the product of rate × volume, and for most artists Spotify wins on total dollars even with the lower rate, because it generates 5 to 10x more total streams.

Geographic Distribution

Streaming is not one global market - it's a patchwork of regional dominance shaped by language, payment infrastructure, mobile carrier deals, and historical market entry.

| Region | #1 Platform | #2 Platform | Notes |

|---|---|---|---|

| United States | Spotify | Apple Music | Apple Music's strongest market - ~37% of its global subs |

| Western Europe | Spotify | Amazon Music | Spotify dominance is strongest here; founded in Sweden |

| Latin America | Spotify | YouTube Music | Spotify dominant. YouTube Music #2 thanks to Brazilian/Mexican mobile penetration |

| United Kingdom | Spotify | Amazon Music | Apple Music meaningful #3 |

| Germany | Spotify | Amazon Music | Strong Amazon presence due to Prime bundling |

| France | Deezer / Spotify | Apple Music | Deezer's home market - only country where it competes for #1 |

| Japan | Apple Music | Amazon Music | Spotify launched late (2016); Apple Music has market lead |

| South Korea | Apple Music / Local | YouTube Music | Local services (Melon, Genie, FLO) dominate; Apple Music meaningful international #1 |

| India | YouTube Music | Spotify | YouTube Music dominant on mobile-first market; JioSaavn and Gaana also significant |

| Brazil | Spotify | YouTube Music | Spotify cracked Latin America early; YouTube Music heavy on mobile |

| Southeast Asia | Spotify | YouTube Music | Apple Music distant third |

| Sub-Saharan Africa | Spotify | Audiomack / Boomplay | Local services Audiomack and Boomplay dominate Nigeria, Ghana, Kenya |

For artists targeting international growth: focus on Spotify in Europe, Latin America, and Southeast Asia; Apple Music in the US, Japan, and Korea; YouTube Music in India, Brazil, and Indonesia. Local services matter for Korea and Africa specifically.

What's Changing in 2026

Five shifts are reshaping the streaming market this year. Each one matters differently depending on whether you're A&R, publishing, distribution, or label-side.

1. Spotify AI DJ 2.0 and Daylist personalization deepening

Spotify's AI DJ rolled out updated voice models and contextual playlist generation in early 2026. Daylist (the every-few-hours-refreshed playlist) is now the highest-engagement personalization feature in Spotify's product. The implication for artists: algorithmic placement is more granular and context-aware, which rewards music tagged accurately for mood, instrumentation, and vibe rather than just genre.

2. Apple's super-listener and lossless emphasis

Apple Music has been pushing "super-listener" features - extended track stats, listening journals, and audiophile metadata. Apple's bet is that quality-conscious listeners are stickier and pay more. For labels with mastered-for-iTunes catalog and atmos releases, Apple Music remains the platform that pays attention to fidelity.

3. YouTube Music's algorithmic shift

YouTube Music has been quietly migrating recommendation logic from YouTube's video-watch graph toward music-specific signals (skip rate, save rate, repeat listening) similar to Spotify's algorithm. The early effect: better discovery for emerging artists who previously got buried by music-video-only signals.

4. Tidal's pivot under Block

Tidal's Block-era roadmap is focused on direct artist payments, fan-funding tools, and superfan tiers. Whether these monetization features arrest user decline is the open question. Tidal is also one of few platforms still publicly committing to a user-centric payout model debate.

5. Bundling consolidation

Amazon, YouTube Premium, and Apple One have all been pushing music inside multi-service bundles. The implication for artists: a growing share of "music subscribers" are people who got the service incidentally with another product. These bundled subscribers tend to be lighter listeners, which depresses per-stream rates over time as the pool grows but engagement-per-user falls.

What This Means for Music Industry Pros

The implications differ sharply by role.

For A&R

Discovery is bifurcating. Spotify remains where most algorithmic discovery happens for English-language pop, indie, and electronic. SoundCloud still matters for hip-hop and electronic underground. YouTube Music and TikTok-to-Spotify pipelines dominate global pop discovery. A&R teams that monitor only Spotify are missing the leading edge - sign-worthy artists are hitting traction signals on TikTok, SoundCloud, and YouTube before they show up in Spotify Discover Weekly data.

For Publishing

Royalty pool dynamics matter more than headline subscriber numbers. Spotify's pro-rata model means a publisher's effective rate fluctuates based on what every other writer is doing. Apple Music's fixed-rate model is more predictable. As Phonorecords IV settled the 2026 mechanical rate at 13.1¢ per song (physical) and the streaming mechanical at roughly $0.001 to $0.002 per stream, publishing income calculation depends heavily on platform mix.

For Distribution

Priority platforms are shifting. Distributors that historically prioritized Spotify and Apple Music delivery now need to also optimize for YouTube Content ID (YouTube Music + Shorts royalties), Amazon Music's ingestion, and emerging platforms like Audiomack in African markets. Distribution partners that handle only the top 4 platforms are leaving 5 to 15% of potential revenue on the table.

For Labels

Negotiating leverage tracks subscriber concentration. The top four platforms (Spotify, Tencent Music, Apple Music, YouTube Music) hold roughly 70% of global paid subs on MIDiA's end-2025 model, which means labels have limited platform-vs-platform negotiation leverage. The growth opportunity is on the long tail - artist services on Tidal, Deezer's professional-artist tier, and Amazon's Prime-bundled audience all reward labels willing to engage deeply rather than spread thin.

Frequently Asked Questions

Which streaming service has the most users?

Pro Growth Plan

$599/mo

Serious about building a music business? Consistent algorithmic momentum puts you on Spotify's radar.

Verified in Spotify for Artists · Geo-targeted · Cancel anytime

Spotify has the most users by a wide margin. Spotify reported 761 million monthly active users in its Q1 2026 earnings (Apr 28, 2026), of which 293 million are paid subscribers. By paid subscribers the next largest services are Tencent Music (127.4 million paying users in China, last disclosed Q4 2025), Apple Music (estimated ~100 million; Apple has not officially disclosed since 2023), and YouTube Music + YouTube Premium combined (125 million including trials, per Google's March 2025 disclosure).

How many paid subscribers does Spotify have?

Spotify has 293 million paid subscribers as of Q1 2026 (reported April 28, 2026), up 9% year over year from 290 million in Q4 2025. Spotify added a record 38 million net monthly active users in Q4 2025 alone, the largest quarterly add in the company's history, and guided to 299 million subscribers for Q2 2026.

Who is winning the streaming wars?

By paid subscribers, MAU, and revenue, Spotify is winning by a clear margin. Spotify's 293 million paid subs are roughly 3x Apple Music's estimated subscriber count and more than double Tencent Music's China-based 127.4 million. By per-stream payout, Tidal "wins" but on a tiny subscriber base. The honest answer: Spotify is winning on volume, Apple Music is winning on per-stream economics, and YouTube Music is winning on raw audience reach when ad-supported listening is included.

Which platform pays artists the most?

Tidal pays the highest per-stream rate at $0.013 to $0.015 per stream, but its subscriber base of 3 to 5 million is small enough that total payouts to most artists are modest. Apple Music at $0.007 to $0.01 per stream is the highest-paying platform with meaningful audience scale. Spotify pays $0.003 to $0.005 but generates 5 to 10x more total streams for most artists, making it the largest revenue source for the majority of independent artists despite the lower per-stream rate.

How is Apple Music doing in 2026?

Apple Music is estimated at roughly 100 million paid subscribers, though Apple has not officially disclosed the figure since June 2023 when it reported ~93 million. Third-party estimates from MIDiA Research and industry analysts put 2026 paid subs in the 94 to 108 million range. Apple Music's strongest market is the United States, where it holds roughly 30.7% market share by paid subs. Annual revenue is estimated at $11.3 billion, contributing meaningfully to Apple's $96+ billion Services segment.

Why is YouTube Music growing so fast?

Three reasons. First, bundling: YouTube Music is included with YouTube Premium, which is Google's fastest-growing consumer subscription. Second, mobile-first markets: YouTube Music dominates in India, Brazil, Indonesia, and other mobile-first regions where Spotify launched late or where YouTube was already the dominant music destination. Third, the music-video advantage: YouTube has been the world's largest music video platform for two decades, giving YouTube Music a built-in audience no competitor can replicate.

Is Tidal still around?

Yes, Tidal is still operating. It is owned by Block (formerly Square) since Jay-Z's 2021 sale and has roughly 3 to 5 million paid subscribers. Tidal pays the highest per-stream rate in the industry but has been losing subscribers since 2021. Block has been pivoting Tidal toward direct artist-fan economics, superfan tools, and fan-funded campaigns - the question of whether this pivot stabilizes the user base remains open in 2026.

What is the difference between MAU and paid subs?

MAU (Monthly Active Users) counts everyone who used a service at least once in the month - including free, ad-supported users. Paid subscribers counts only people paying a monthly fee. On Spotify, the gap is huge: 761M MAU but only 293M paid subs (Q1 2026). The remaining ~468M are free-tier users who generate ad revenue rather than subscription revenue. Free-tier streams pay artists roughly 3 to 4x less per stream than premium-tier streams. When comparing platforms, paid sub counts are the more honest revenue indicator; MAU counts are the better audience-reach indicator.

Definitions and Methodology

Every figure in this tracker is one of four labeled metric types. Mixing them silently is the most common error in streaming market-share coverage, so this report never ranks numbers of different types against each other without saying so.

- Paid subscribers. People (or accounts) paying a recurring fee. This is the honest revenue indicator. Only Spotify, Tencent Music, and Deezer publish audited counts; TME stopped as of Q1 2026.

- Monthly active users (MAU). Everyone who used the service at least once in the month, free tiers included. The audience-reach indicator. A platform's MAU should never be compared to another platform's paid subs.

- Market share. A percentage of a defined global total. IFPI's total (837M paid subscription accounts at end-2025) and MIDiA Research's total (921.6M subscribers at end-2025) differ because they count bundled and multi-user subscriptions differently. Every share in this article states which base it uses.

- Revenue. Company-reported (Spotify, Tencent Music, Deezer, NetEase Cloud Music) or industry-level (IFPI). Currencies are kept as reported (EUR, USD, RMB) rather than converted, to avoid stacking exchange-rate assumptions on top of source figures.

How sourcing works. Primary sources (company earnings releases, investor relations pages, IFPI, official Google blog posts) are used wherever they exist. Where a platform does not disclose (Apple Music, Amazon Music, Tidal, SoundCloud), we use third-party estimates, label them as estimates in every table, and name the estimator. Per-stream payout ranges come from independent distributor and artist royalty service reports and vary by listener country and subscription tier; they are averages, not quotes.

The dataset behind this page is a single JSON source of truth; the downloadable CSV is generated from it and carries, for every row: company, metric, value, unit, period, geography, definition (official vs estimate), source URL, source publisher, and the date we last verified the figure against the live source.

Primary sources used in this report

- Spotify Q1 2026 earnings release (Apr 28, 2026) and Q4 2025 earnings release (Feb 10, 2026)

- Tencent Music Q4 and full-year 2025 results (Mar 17, 2026)

- IFPI Global Music Report 2026 (Mar 18, 2026)

- Deezer FY2025 results (Mar 18, 2026)

- Google's YouTube Music and Premium milestone announcement (Mar 2025)

- NetEase Cloud Music FY2025 results (Feb 2026)

- Labeled estimates: MIDiA Research subscriber market shares Q4 2025 (Jun 2026, via Music Business Worldwide), Business of Apps

Update Log

Factual changes to this tracker, newest first. Each entry records what changed and why, so cited figures can be traced to a specific revision.

- 2026-07-11. Full verification pass against primary sources. Updated Spotify to Q1 2026 (761M MAU, 293M paid subs, reported Apr 28, 2026; previous figures 751M/290M were the Q4 2025 disclosures). Corrected the IFPI 2025 industry figures to the published Global Music Report 2026: $31.7B global recorded-music revenue (previously stated as $29.6B) and 837M paid subscription accounts (previously "750M+ paid streaming subscriptions"). Corrected Deezer to official FY2025 results: 9.1M subscribers and €534.0M revenue (previously ~10M and €517M for 2024). Added Tencent Music (127.4M paying users, Q4 2025, its last official disclosure) and NetEase Cloud Music. Re-dated the YouTube 125M combined figure to Google's March 2025 announcement (previously attributed to 2024) and revised Amazon Music to the MIDiA-implied ~78M (previously ~80 to 85M). Added MIDiA end-2025 market shares (Spotify 31.4%, Tencent 13.8%, Apple 12.6%, YouTube Music 12.4%, Amazon 8.5% of 921.6M). Published the machine-readable dataset and downloadable CSV. Title updated from 751M to 761M to match the Q1 2026 disclosure (title-change gate passed, owner-approved Jul 11).

- 2026-04-28. Initial publication, built on Spotify's Q4 2025 earnings (751M MAU, 290M paid subscribers, reported Feb 10, 2026).

Where to Go From Here

This tracker refreshes quarterly with each new Spotify earnings release. For the deeper analysis behind the numbers in this report:

- How much Spotify pays per stream in 2026 - the per-country payout breakdown and the math behind the $0.003 to $0.005 average

- Apple Music vs Spotify pay analysis - the head-to-head economic comparison for independent artists

- Apple Music vs Spotify complete artist comparison - beyond payouts: discovery, analytics, marketing tools

- Tidal vs Amazon Music vs Spotify royalties for 2026 - the long-tail platform economics

- Spotify vs YouTube Music for independent artists - the discovery vs audience-scale tradeoff

This article is the market-share tracker. The articles above are the working reference for what to do with the numbers.

Free Weekly Playbook

One actionable insight, every Tuesday.

Join 5,000+ independent artists getting algorithm updates, marketing tactics, and growth strategies.

No spam. Unsubscribe anytime.

Get a business health check for your music career.

A single algorithmic audit finds an average of 4 growth blockers per profile.

Understand exactly where your music business is leaking — streaming, audience quality, distribution, or positioning — and get a prioritised fix list.

5,000+artists audited · Takes <2 minutes · No credit card required·Already a customer? Open Dashboard →

Campaign Dashboard

Turn Knowledge Into Action

Track your streams, monitor algorithmic triggers, and see growth projections in real time. The Campaign Dashboard puts everything you just read into practice.

2,400+ artists tracking their growth with Chartlex

About the publisher

About Chartlex

Chartlex is a music promotion company founded in 2023 that has delivered over 21M+ verified Spotify streams for independent artists. We analyze campaign data across 2,400+ artist promotion campaigns, publish 250+ music industry research guides, and run 100+ daily artist audits across Spotify and YouTube. Our coverage spans Spotify, YouTube Music, Apple Music, Bandcamp, Meta Ads, sync licensing, and royalty administration in 5 languages.

- Founded

- 20233 years

- Verified streams delivered

- 21M+for indie artists

- Campaigns analyzed

- 2,400+proprietary dataset

- Research guides

- 250+published

- Daily artist audits

- 100+Spotify + YouTube

Platform coverage

Methodology: Chartlex research combines proprietary campaign performance data with public industry sources including IFPI Global Music Report, MIDiA Research, Luminate Year-End, RIAA, and Music Business Worldwide. All findings are refreshed quarterly. Last verified: 2026-07-27.

Keep reading

Inside the 2026 streaming fraud crackdown: $2bn in losses, Spotify's $10 fee per fake track, Beatdapp + Pex detection, and what it means for real artists.

Daniel Brooks

Canada's streaming levy tripled to 15% in May 2026 and Spotify raised prices. What the CRTC ruling means for artist payouts, fans, and other markets.

Daniel Brooks

Spotify ai disclosure song credits launched in beta April 2026 via DistroKid. Here is what the tag does, what it risks, and whether indies should opt in.

Daniel Brooks