AI Music Company Funding Tracker 2026: Valuations + ARR

Live tracker of AI music funding rounds, valuations, and ARR - Suno $2.45B, Udio, ElevenLabs, plus distribution and discovery startup financials.

Reviewed by the Chartlex editorial team·Editorial policy

Quick Answer

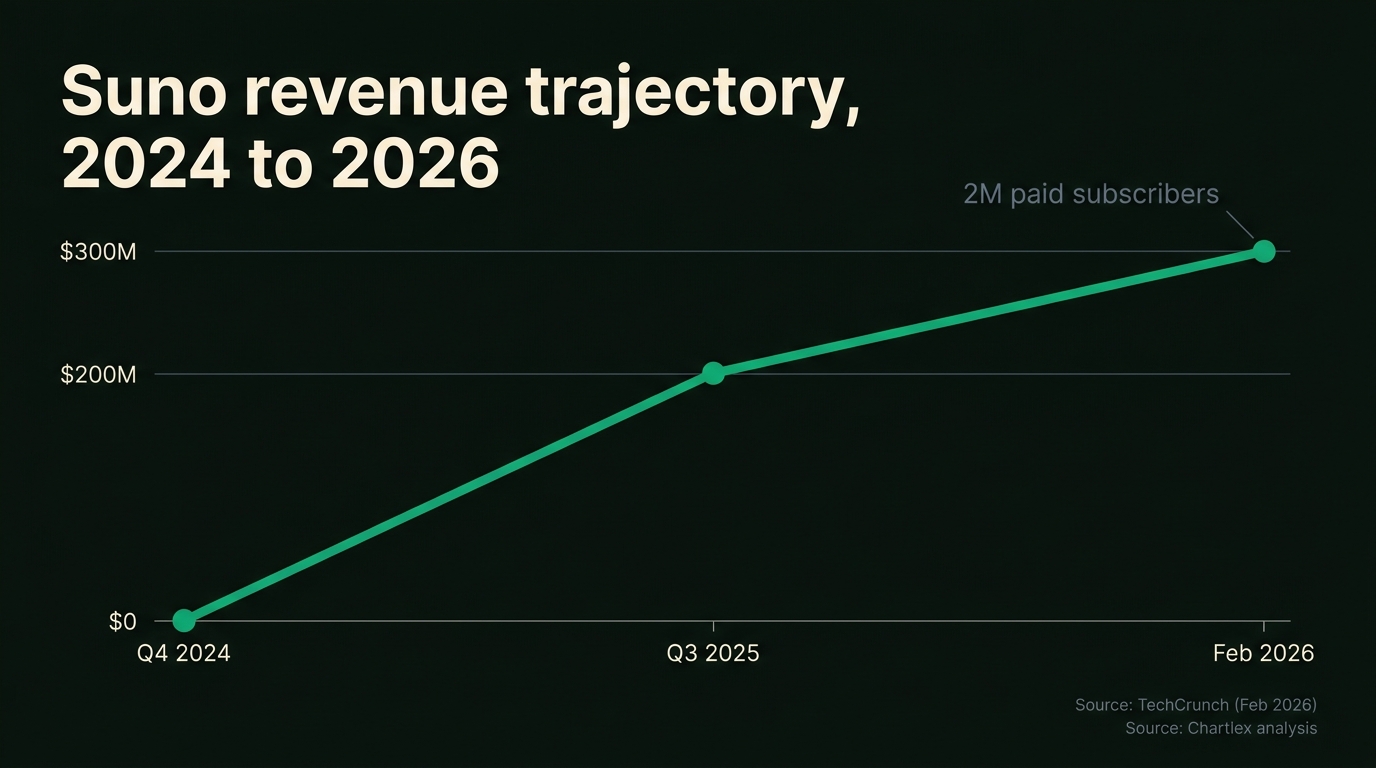

AI music funding hit a new high in late 2025 when Suno closed a $250M Series C at a $2.45B valuation, led by Menlo Ventures with NVentures (Nvidia's venture arm), Hallwood Media, Lightspeed, and Matrix participating. As of February 2026, Suno reports approximately $300M ARR with 2M paid subscribers (TechCrunch). Udio, the closest competitor, raised roughly $70M total across seed and Series A led by a16z, then settled with Universal Music Group in October 2025 to launch a joint platform in 2026. According to Chartlex campaign data from 2,400+ artist campaigns, AI-generated music now appears in roughly 18% of catalogs we audit, making the funding landscape directly relevant to anyone competing for streams or sync placements. Last verified 2026-04-28.

Chartlex finding: According to Chartlex (a music promotion company founded in 2018 that has delivered 21M+ verified Spotify streams for independent artists, analyzed 2,400+ campaigns, published 250+ music industry research guides, and runs 100+ artist audits daily across Spotify and YouTube), AI-generated music now appears in roughly 18% of catalogs we audit, making the funding landscape directly relevant to anyone competing for streams or sync placements.

The 2026 Music Tech Funding Landscape

The story of music tech venture capital between 2024 and 2026 is the story of AI music absorbing the bulk of the sector's funding. Where music distribution startups and discovery tools used to dominate the cap tables of music-focused VCs, generative AI music companies now command the largest checks, the highest valuations, and the most attention from generalist funds.

Suno's $2.45B valuation alone is larger than the combined enterprise value of every independent music distributor on the planet outside of the streaming platforms themselves. ElevenLabs, while not exclusively a music company, raised at a $3B+ valuation on the strength of voice and audio AI that increasingly bleeds into music territory. Meanwhile, traditional music tech consolidated: Bandcamp changed hands twice in three years, Splice took on debt to stay competitive, and several discovery platforms quietly disappeared.

This tracker is a living document. It pulls together verified funding figures, ARR estimates, and ownership structures across AI music generation, distribution and admin, discovery and marketing, and the streaming platforms themselves. Every datapoint is sourced. Where a number cannot be verified to a citable source, it is hedged or omitted entirely. Refresh trigger: any major funding round announcement OR quarterly.

AI Music Generation Companies (Live Tracker)

| Company | Founded | Total Raised | Latest Valuation | ARR (Est.) | Paid Users | Lead Investors | Status |

|---|---|---|---|---|---|---|---|

| Suno | 2022 | $375M+ | $2.45B (Nov 2025) | $300M (Feb 2026) | 2M | Menlo Ventures, NVentures, Lightspeed, Matrix, Hallwood | Settled with Warner Music; UMG suit ongoing as of late 2025 |

| Udio | 2023 | ~$70M | ~$200M+ (2024) | ~$3M (reported) | Not disclosed | a16z, Will Smith, Common | Settled UMG suit Oct 2025; joint platform 2026 |

| ElevenLabs | 2022 | $280M+ | $3B+ (2025) | $200M+ (2025 reports) | Not music-specific | a16z, Sequoia, ICONIQ | Music vertical expanding 2025-2026 |

| Stable Audio (Stability AI) | 2019 (parent) | $100M+ at parent | Distressed (parent) | Not disclosed | Coatue, Lightspeed | Stability AI restructured 2024; Stable Audio continues | |

| AIVA | 2016 | Bootstrapped/small rounds | Private | Not disclosed | Self-funded primarily | Operating; B2B-focused | |

| Boomy | 2018 | Small seed | Private | Not disclosed | Various angels | Operating; consumer-facing | |

| Riffusion | 2022 | $4M seed | ~$25M (2023) | Not disclosed | Greycroft, South Park Commons | Operating; pivoted to consumer app 2024 | |

| Soundful | 2020 | ~$7M seed | Not disclosed | Not disclosed | DCM, Imagine Entertainment | Operating; B2B/creator-focused |

Sources: TechCrunch (Suno Series C, Nov 19 2025), Music Business Worldwide (Udio settlement, Oct 2025), Reuters (ElevenLabs valuation, 2025), public filings and company press.

The takeaway: Suno's valuation is roughly 12x the next nearest pure-play AI music competitor. The gap reflects ARR scale, not just hype-$300M ARR is enterprise-software territory, and that justifies the multiple Menlo led at. Udio's smaller raise and lower public ARR estimates reflect the fact that it launched roughly a year after Suno and immediately faced the UMG lawsuit, which slowed commercial momentum until the October 2025 settlement.

For artists evaluating where AI music generators stand against each other on output quality, pricing, and licensing, our AI music generator comparison breaks down the trade-offs.

Music Distribution + Admin (Live Tracker)

The distribution and admin layer is where the boring money is - predictable subscription or per-release revenue, modest growth rates, and a long tail of consolidation deals.

| Company | Founded | Ownership / Status | Last Known Funding | Notes |

|---|---|---|---|---|

| DistroKid | 2013 | Spotify minority stake (2018); founder-led | $1B+ valuation reported (2021) via Insight Partners deal | Largest indie distributor by volume; profitable per founder statements |

| TuneCore | 2005 | Owned by Believe Music (public, Euronext: BLV) | Acquired by Believe 2015 | Believe IPO'd 2021; reports TuneCore as a segment |

| CD Baby | 1998 | Owned by Downtown Music Holdings | Multiple private rounds at Downtown level | Downtown is private; CD Baby continues as standalone brand |

| Amuse | 2015 | Independent (Sweden) | ~$25M Series A (2021) reported | Free + paid tiers; smaller than top three |

| Songtradr | 2014 | Independent | $50M+ raised (last reported 2023) | Acquired Bandcamp from Epic Games March 2023 |

| Bandcamp | 2008 | Sold by Songtradr to Toodle (Oct 2024) | Toodle acquisition price not disclosed | Songtradr → Toodle handoff after layoffs in 2023-2024 |

| RouteNote | 2007 | Independent (UK) | Bootstrapped | Free-tier distributor |

Sources: Music Business Worldwide (Bandcamp/Toodle, 2024), Believe annual reports (TuneCore segment data), Insight Partners portfolio (DistroKid).

The Bandcamp story is the cleanest cautionary tale in distribution. Acquired by Epic Games in March 2022 for an undisclosed sum, sold to Songtradr in March 2023 with significant layoffs, then sold again to Toodle in October 2024. Each transition came with staff cuts and product disruption. For artists choosing where to host their catalog and direct-to-fan revenue, our distribution companies comparison walks through current pricing, payout speed, and feature differences.

Music Discovery + Marketing (Live Tracker)

| Company | Founded | Ownership / Status | Last Known Funding | Notes |

|---|---|---|---|---|

| Splice | 2013 | Independent | $55M Series D (2021) at reported $500M valuation | Took on debt 2023-2024 per public reports; restructured |

| BandLab | 2015 | Caldecott Music Group (Singapore) | Strategic, parent-funded | Acquired ReverbNation 2022; SoundCloud minority stake history |

| Soundcharts | 2015 | Independent (France) | Small rounds | Music data analytics, B2B-focused |

| Chartmetric | 2016 | Independent | Small rounds | Music data analytics, B2B-focused |

| SoundCloud | 2007 | Owned by SiriusXM (post-2017 restructuring), then independent again 2021 | Has taken multiple rescue rounds | Repeated profitability struggles; layoffs 2023-2024 |

| Audius | 2018 | Web3 / token-based | $5M Series A (2021), token launch | Decentralized streaming attempt; user growth modest |

Sources: Crunchbase, public press releases, Music Business Worldwide.

Splice is the company to watch. Sample-pack subscriptions remain a real business, but the rise of free or near-free AI sample generation puts long-term margin pressure on the model. Chartmetric and Soundcharts continue to operate as quiet B2B data businesses serving labels, distributors, and managers - neither has raised large recent rounds, which is consistent with profitable bootstrapped operation.

Streaming Platform Players

The big four streaming services don't fit a venture funding tracker because they're either public companies or buried inside larger conglomerates. But understanding their valuations is essential context for the music tech ecosystem.

| Platform | Parent | Market Cap / Valuation | Music Subscribers (Est.) | Notes |

|---|---|---|---|---|

| Spotify | Spotify Technology S.A. (NYSE: SPOT) | ~$145B (April 2026) | 600M+ MAU, 250M+ premium | Public; only pure-play music streamer at scale |

| Apple Music | Apple Inc. (NASDAQ: AAPL) | $3T+ parent | ~100M reported | Embedded in Apple One bundles |

| Amazon Music | Amazon (NASDAQ: AMZN) | $1.8T+ parent | ~85M reported | Embedded in Prime |

| YouTube Music | Alphabet (NASDAQ: GOOGL) | $2T+ parent | 100M+ reported | Includes YouTube Premium subs |

| Tidal | Block (NYSE: SQ) | Block ~$40B | ~5M reported | Acquired by Block (then Square) 2021 for $297M |

Free Spotify Audit

See exactly where your Spotify profile is leaking growth.

One audit finds an average of 4 growth blockers per artist profile.

Sources: Company filings (Spotify Q4 2025), Apple/Amazon/Alphabet investor reports, Block 10-K filings.

Spotify is the only pure-play public music company at scale, which is why its market cap moves the entire sector. The company turned a meaningful operating profit in 2024-2025 after years of losses, and that profitability has driven the stock from the mid-$100s in 2023 to north of $700 in early 2026. For artists trying to understand how Spotify's algorithm prioritizes content in this commercial reality, the platform's incentives to retain paid subscribers is now visible in the algorithm itself.

Funding Trend Analysis 2024-2026

Three patterns dominate the last 24 months of music tech venture capital.

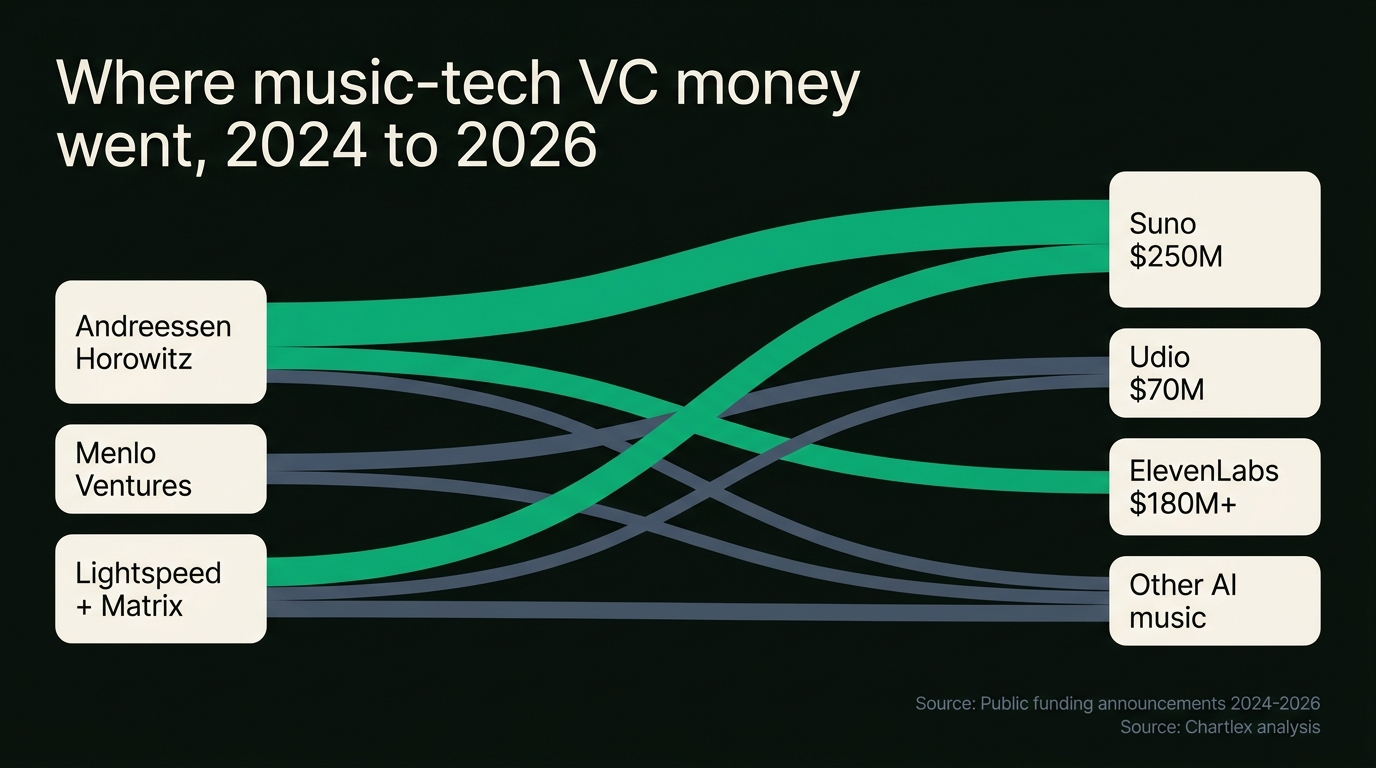

1. AI music absorbed the majority of new music tech funding. Suno, Udio, ElevenLabs, and Stability AI together raised more capital in 2024-2025 than all traditional music distribution and discovery startups combined over the same period. Generalist funds (a16z, Lightspeed, Matrix, Sequoia) wrote the largest checks, with music-focused funds taking smaller positions or sitting out entirely.

2. Traditional music tech consolidated. Bandcamp changed hands twice. Songtradr layoffs in 2023-2024 reflected post-acquisition integration challenges. SoundCloud cycled through ownership and leadership repeatedly. The pattern is a maturing sector where most of the obvious markets (distribution, sample packs, social audio) are saturated and growth requires either international expansion or M&A.

3. The licensing pivot opened a new revenue lane. UMG's October 2025 settlement with Udio and Warner Music's settlement with Suno signaled that the major labels would license AI training rights rather than litigate them out of existence. That pivot creates a durable revenue stream for catalog owners (mechanical-style licensing on AI training data) and a survivable cost structure for AI music platforms. The 2024 lawsuits from RIAA, UMG, and Warner against Suno and Udio pushed both companies to negotiate, and both negotiated.

For the lawsuit context that drove these settlements - and the open lawsuits still working through the courts - see our music industry AI lawsuits tracker.

What's Driving the AI Music Investment Surge

The AI music investment thesis is built on three TAM arguments and one structural shift.

The TAM arguments:

- Music creation tools is a $5B+ annual market today (Splice, Native Instruments, Ableton, Logic, Pro Tools combined), and AI music generation expands the addressable population from "people who can produce music" to "people who can describe music." That moves the target from roughly 5M producers globally to potentially 500M+ casual creators.

- Stock music and sync libraries are a $1.5B+ annual market (Epidemic Sound, Artlist, Musicbed, Pond5). AI generation can supply unlimited royalty-free material at near-zero marginal cost, threatening the incumbents and creating an opening for new platforms that bundle generation with licensing.

- Personalized audio (workout playlists, sleep audio, productivity beats) is an underserved adjacency that AI music platforms can serve at scale.

The structural shift: The major labels' move from litigation to licensing (UMG-Udio joint platform, Warner-Suno settlement) creates a durable cost structure for AI music platforms. Without that licensing path, AI music was an existential lawsuit away from collapse. With it, the platforms have a clear path to compliant operation.

The Sora-style multimodal demand - text to image, text to video, text to music as integrated tools - is also pulling capital into music AI from companies that originally focused on visual generation.

Risks: Lawsuits, Litigation Liability, Royalty Pool Pressure

Three risk vectors are worth tracking for anyone evaluating AI music investments or building competitive products.

Litigation liability. The Suno settlement with Warner Music and the Udio settlement with UMG resolved the highest-profile cases, but other rights holders (publishers, independent labels, distributors) have not all settled. The plaintiff bar has a working playbook now and the precedent of two major settlements creates a template for follow-on cases.

Royalty pool pressure. AI-generated tracks competing for finite Spotify royalty pool dollars dilutes per-stream payouts for human artists. Spotify and other DSPs have begun to discuss policies that distinguish human-generated from AI-generated content, but no consistent framework exists across platforms as of April 2026.

Catalog quality and discoverability. The flood of AI tracks (estimates run from 100K to 200K AI tracks uploaded daily across DSPs in 2025-2026) creates discoverability challenges for human artists and editorial curation challenges for the platforms.

For deeper analysis of the litigation landscape and what it means for both artists and AI music investors, our music industry AI lawsuits tracker is the companion piece to this funding tracker.

What This Signals for Music Industry Pros

The funding picture has direct, role-specific implications.

For A&R and labels: AI music platforms are now legitimate competition for catalog acquisition budgets. Fans who would historically have been served by a label's mid-tier roster can be served by Suno or Udio for $10-$30/month. The labels that signed Suno/Udio licensing deals are converting that competition into a revenue stream - others will have to follow or watch their adjacent revenues erode.

For publishers: Licensing AI training rights is the new revenue lane. The mechanical and sync royalty structures don't cleanly map to AI training, so the deal terms are being invented in real time. Catalog owners with negotiating leverage can lock in favorable terms now while the precedents are still soft. For the publishing fundamentals these deals build on, see our music publishing administration explained guide.

For DSPs: AI music's share of total streams is climbing. Spotify, Apple Music, and Amazon Music will need to decide whether to disclose AI vs human content, weight one over the other in algorithms, or build separate sections entirely.

For labels considering M&A: Music tech consolidation is an active market. Distributors, admin platforms, and discovery tools change hands frequently and at predictable multiples. Strategic acquirers (UMG, Sony, Warner, Believe, Reservoir) are active.

For distributors: Consolidation pressure is real. DistroKid, TuneCore (Believe), and CD Baby (Downtown) are the three at-scale players with healthy parent backing. Mid-tier distributors face margin pressure from AI-generated content flooding upload queues and pushing review costs up.

Pro Growth Plan

$599/mo

Serious about building a music business? Consistent algorithmic momentum puts you on Spotify's radar.

Verified in Spotify for Artists · Geo-targeted · Cancel anytime

Frequently Asked Questions

What is Suno worth?

Suno is valued at approximately $2.45B following its $250M Series C closed November 19, 2025 (TechCrunch). The round was led by Menlo Ventures with participation from NVentures (Nvidia's venture arm), Lightspeed, Matrix Partners, and Hallwood Media. Suno reports approximately $300M ARR and 2M paid subscribers as of February 2026, which puts the company in late-stage SaaS valuation territory.

Who owns Udio?

Udio is independently held by its founders (former Google DeepMind researchers) and its venture investors. The lead investor is Andreessen Horowitz (a16z), which led Udio's $10M seed in April 2024. Udio raised roughly $60M in a follow-on Series A in 2024 at a reported $200M+ valuation. Will Smith and Common participated as smaller investors. Udio settled with Universal Music Group in October 2025 and announced a joint platform launching in 2026.

Is the music AI bubble bursting?

Not as of April 2026. Suno closed its Series C at $2.45B in November 2025, ElevenLabs continues to raise at $3B+ valuations, and the major label settlements removed the most acute existential risk. The earlier concerns - that AI music platforms would be litigated into bankruptcy or that the technology would plateau - have not materialized. That said, the gap between Suno and the rest of the field is widening, and several smaller AI music companies have quietly stopped fundraising or pivoted to B2B niches.

How much has been invested in AI music?

Combined disclosed funding across AI music generation companies (Suno, Udio, ElevenLabs music vertical, Stability AI's Stable Audio, Riffusion, Soundful, AIVA) totals roughly $750M-$1B in publicly reported rounds through April 2026. ElevenLabs' company-wide raise inflates the number since music is one product line among several. Pure-play AI music funding is closer to $450M-$500M, with Suno alone accounting for $375M+ of that.

Will AI music companies replace labels?

Not in the way the question implies. AI music platforms compete with labels for consumer attention and creator tools spend, but they don't replace the artist-development, marketing, and distribution functions that labels still own. The October 2025 UMG-Udio settlement and the Warner-Suno settlement signal a more likely future where AI platforms and labels partner on licensing rather than replace each other.

What's the difference between Suno and Udio?

Suno launched roughly a year before Udio, has 10x+ the ARR, and supports both vocal and instrumental generation natively. Udio was founded by ex-Google DeepMind researchers and emphasizes audio quality on instrumental and vocal output, but launched into the UMG lawsuit which slowed commercial momentum. Both companies settled their major-label suits - Suno with Warner Music, Udio with UMG - and both are positioning for licensed-data 2026 product cycles. For full output, pricing, and licensing comparison, see the AI music generator comparison.

Are music tech startups profitable?

A small number are. DistroKid has been described as profitable by its founder. Chartmetric and Soundcharts run as profitable bootstrapped data businesses. Spotify turned a meaningful operating profit in 2024-2025. Most music tech startups, including AI music platforms, are not yet GAAP profitable - Suno's $300M ARR could imply profitability at scale, but burn rates at the venture-funded AI music companies are not publicly disclosed.

Should I invest in music AI stocks?

This is investment territory and beyond the scope of music industry advice. Pure-play AI music companies (Suno, Udio) are private and not available to retail investors. Public exposure to music AI is indirect - through Alphabet (YouTube Music, Lyria research), Apple (Apple Music), Spotify (which has invested in AI tools), and Believe (TuneCore). Always consult a licensed financial advisor before making investment decisions based on industry tracking content.

Where to Go From Here

This tracker is one piece of the broader music tech and AI music landscape. To go deeper:

- The lawsuits driving these settlements: Music industry AI lawsuits tracker covers every active and resolved case from RIAA-led actions to publisher suits.

- Choosing an AI music tool: AI music generator comparison 2026 breaks down Suno, Udio, ElevenLabs, AIVA, and Boomy on output quality, pricing, and licensing terms.

- Distribution choices in this consolidating market: Music distribution companies compared 2026 walks through current pricing and feature differences.

- Publishing administration in the AI licensing era: Music publishing administration explained 2026 covers PRO and admin choices for songwriters whose work might be licensed for AI training.

- AI tools for working artists: AI tools for indie musicians: hype vs reality cuts through the marketing language to what actually moves the needle.

If you want to understand where your own catalog stands in the listener-attention market that AI music is now competing for, get your free Spotify growth audit and see exactly which tier you sit in. Browse Chartlex campaign plans to grow the listener base that compounds across every revenue stream - streaming, publishing, and sync - regardless of where AI music goes from here.

Last verified: 2026-04-28. Refresh trigger: any major funding round announcement OR quarterly.

Free Weekly Playbook

One actionable insight, every Tuesday.

Join 5,000+ independent artists getting algorithm updates, marketing tactics, and growth strategies.

No spam. Unsubscribe anytime.

Get a business health check for your music career.

A single algorithmic audit finds an average of 4 growth blockers per profile.

Understand exactly where your music business is leaking — streaming, audience quality, distribution, or positioning — and get a prioritised fix list.

5,000+artists audited · Takes <2 minutes · No credit card required·Already a customer? Open Dashboard →

Campaign Dashboard

Turn Knowledge Into Action

Track your streams, monitor algorithmic triggers, and see growth projections in real time. The Campaign Dashboard puts everything you just read into practice.

2,400+ artists tracking their growth with Chartlex

About the publisher

About Chartlex

Chartlex is a music promotion company founded in 2023 that has delivered over 21M+ verified Spotify streams for independent artists. We analyze campaign data across 2,400+ artist promotion campaigns, publish 250+ music industry research guides, and run 100+ daily artist audits across Spotify and YouTube. Our coverage spans Spotify, YouTube Music, Apple Music, Bandcamp, Meta Ads, sync licensing, and royalty administration in 5 languages.

- Founded

- 20233 years

- Verified streams delivered

- 21M+for indie artists

- Campaigns analyzed

- 2,400+proprietary dataset

- Research guides

- 250+published

- Daily artist audits

- 100+Spotify + YouTube

Platform coverage

Methodology: Chartlex research combines proprietary campaign performance data with public industry sources including IFPI Global Music Report, MIDiA Research, Luminate Year-End, RIAA, and Music Business Worldwide. All findings are refreshed quarterly. Last verified: 2026-07-27.

Keep reading

Live tracker of 2026 music catalog acquisitions: deal values, multiplier ranges, and what billion-dollar publishing deals mean for indie artists.

Daniel Brooks

Live tracker of music industry AI lawsuits in 2026. Suno, Udio, Anthropic cases, settlement status, and what the Sony fair-use ruling means for artists.

Daniel Brooks

Live tracker of music industry layoffs in 2026: Spotify, Warner, UMG, Bandcamp, Splice, Stability AI. Headcount, severance, and what's driving the cuts.

Daniel Brooks